Have questions about your mortgage?

Understanding the mortgage financing process can be difficult. It doesn't have to be when you follow my 3 step plan.

Get started right away

The best place to start is to connect with me directly. The mortgage process is personal. My commitment is to listen to all your needs, assess your financial situation, and provide you with a clear plan forward.

Get a clear plan

Sorting through all the different mortgage lenders, rates, terms, and features can be overwhelming. Let me cut through the noise, I'll outline the best mortgage products available, with your needs in mind.

Let me handle the details

When it comes time to arranging your mortgage, I have the experience to bring it together. I'll make sure you know exactly where you stand at all times. No surprises. I've got you covered.

What clients say about working with me

Everything you need, all in one place

As a trusted mortgage provider, I can help you with these services.

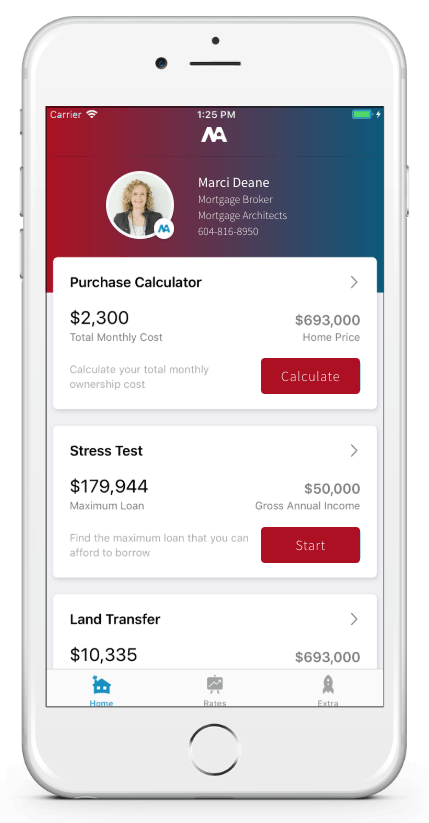

Download My Mortgage Toolbox

What can you do with my app:

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese

55+ and looking for solutions to enhance your lifestyle?

I offer multiple options including Reverse Mortgages, HELOC, standard and private financing to find the right retirement mortgage option for you.

Have You Got Questions About Reverse Mortgages?

I have a place dedicated to explaining the reverse mortgage process!

Latest Blog Articles